LEAPS Calendar Spreads

What Are LEAPS Calendar or Time Spreads?

What are LEAPS Calendar or Time Spreads, and why should you care?

(Recall that LEAPS are basically options that don't expire for a long time - you can learn more about them here.)

A calendar or time spread is an option spread where the different legs of the trade have different expiration dates.

For example, you could:

>> Buy a $50 long call LEAPS option that doesn't expire for a year or two

>> Write or sell a $50 call that expires next month

What's the Rationale for LEAPS Calendar Spreads?

The rationale for the trade can be viewed a couple of different ways.

You might view the premium you receive from selling the near dated option as a reduction of the cost basis on your long dated LEAPS.

After all, if you set up the spread as a single transaction, you're basically placing your limit order as a debit spread where you pay the price of the long call LEAPS less the premium received from the near dated call.

Another way to view the trade is as a way to generate short term income (from repeatedly selling near dated calls) against a longer term asset (i.e. the long call LEAPS).

This is the primary way I view, treat, and set up my LEAPS based calendar spreads.

Let's look at this approach more closely . . .

Like Covered Calls on Steroids

If you understand covered calls, you already have the foundation in place for income-oriented calendar spreads.

Instead of writing covered calls against shares of stock, you can use LEAPS options as a proxy and repeatedly write near dated call options against the LEAPS.

There are two key structural advantages built into these kind of trades.

First, there's a serious Leverage Advantage. Put simply, you can control a whole lot more shares via long LEAPS compared to the capital required to own the shares outright.

How much leverage that turns out to be is going to depend on a lot of factors, including the strike price of the LEAPS you're working with.

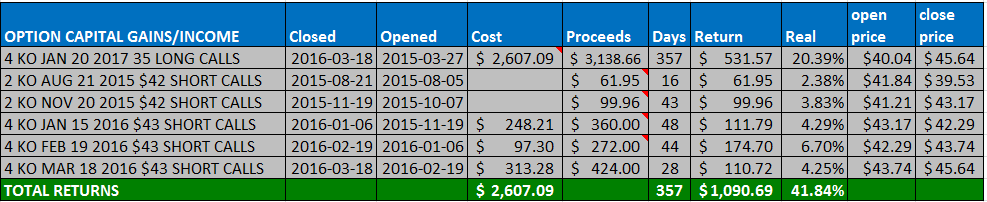

But, by way of illustration, here's an example involving KO where the leverage ratio was roughly 6:1.

{kind=link}

For the same cost of 100 shares of the underlying stock, I could "control" 600 shares by buying 6 long call LEAPS contracts at the $35 strike while the stock itself traded right around $40/share.

Technically, my position was smaller than that, but the ratio was still the same. I controlled 400 shares via 4 long call LEAPS which cost me just $2607.09 in capital to acquire, or equivalent to about 65 shares.

Imagine buying 100 shares of stock and then being allowed to write not just one covered call against those shares, but six! It's not too hard to see the attraction, is it?

There's also a second advantage - the Theta Advantage. A key component to option pricing is that when it comes to decaying time value, theta is much lower the farther away expiration is, and it's much higher the closer expiration is.

Theta also takes on parabolic attributes - the closer expiration gets, the more that rate of daily time decay in an option accelerates.

Again, this is another tailwind for LEAPS based calendar spread traders.

For example, if you're "long" an asset that loses $10/day in value, but you're simultaneously "short" an asset that loses $50/day in value, you're probably going to be very happy with your decaying asset.

All else being equal, that's a "spread" that's making you $40/day.

What About Long Put LEAPS Calendar Spreads?

You're not limited to only using long call LEAPS to set up calendar or time spreads.

You can also construct the spread with long put LEAPS, buying a put option contract that doesn't expire for a year or more and then selling near dated puts against your long position - again, as a way to lower your cost basis on your long put position, or as a way to (hopefully) repeatedly generate income.

In fact, there's nothing preventing you from establishing both call based and put based LEAPS calendar spreads simultaneously on the same underlying stock.

That's actually the basis for an income strategy I teach inside The Leveraged Investing Club called The LEAPS Perpetual Income Strategy.

The trade is designed to eliminate the underlying share price as a factor - at least in terms of the overall value of the long LEAPS.

That's because the call LEAPS and the put LEAPS basically offset one another. The more the one set loses intrinsic value, the more the other set gains intrinsic value.

And then we just repeatedly sell - and manage - near dated calls and puts for lots of income.

Tweet

Follow @LeveragedInvest

HOME : LEAPS Option Strategies : LEAPS Calendar Spreads

![]()

>> The Complete Guide to Selling Puts (Best Put Selling Resource on the Web)

>> Constructing Multiple Lines of Defense Into Your Put Selling Trades (How to Safely Sell Options for High Yield Income in Any Market Environment)

Option Trading and Duration Series

Part 1 >> Best Durations When Buying or Selling Options (Updated Article)

Part 2 >> The Sweet Spot Expiration Date When Selling Options

Part 3 >> Pros and Cons of Selling Weekly Options

>> Comprehensive Guide to Selling Puts on Margin

Selling Puts and Earnings Series

>> Why Bear Markets Don't Matter When You Own a Great Business (Updated Article)

Part 1 >> Selling Puts Into Earnings

Part 2 >> How to Use Earnings to Manage and Repair a Short Put Trade

Part 3 >> Selling Puts and the Earnings Calendar (Weird but Important Tip)

Mastering the Psychology of the Stock Market Series

Part 1 >> Myth of Efficient Market Hypothesis

Part 2 >> Myth of Smart Money

Part 3 >> Psychology of Secular Bull and Bear Markets

Part 4 >> How to Know When a Stock Bubble is About to Pop