Option Trading Strategies for Dividend Growth Investors

How Options Can Accelerate the Dividend Growth Process

This is Part 2 of a 3 part series on option strategies for different investors:

- Option Strategies for High Yield Income Investors

- Option Strategies for Value Investors

- Option Strategies for Dividend Growth Investors (You Are Here!)

In a separate article, I talk about how a value investing with options approach could solve the biggest problem value investors face - bridging the gap between quality and price.

We all know that great companies seldom go on significant sale - unless something terrible happens to them or the market in general.

Value investing with options - as I teach and advocate it - is designed to realize the dream that most value investors have given up on - the acquisition of exceptional businesses at exceptional prices.

Options and Dividend Growth Investing

But what if you're more of a dividend growth investor than a value investor?

Can the same value investing with options approach help you solve your primary problem?

And just what is your primary problem anyway?

Dividend growth investing (DGI) is very simple.

When you own shares of companies that increase their dividends every year - and there are many that do just that - your dividend income can really grow over time.

And, given enough time, in ways that can be truly astounding.

Companies like Coca-Cola and Procter & Gamble, for example, have increased the amount they pay out in dividends each year for more than 50 years in a row.

(They can afford to do so because, over time, they continue to increase their earnings.)

And, over time, those dividends (and dividend yields) can really add up.

I could cite any number of specific and crazy examples of what would have happened had you bought shares of Procter & Gamble, Walmart, McDonald's, Coca-Cola, Johnson & Johnson, etc. at some point in the past and done nothing but held the shares until present day.

But here's a simple example that makes the point:

In 2013, Daily Trade Alert reported that the Coca-Cola shares that Warren Buffett purchased for Berkshire-Hathaway back in the late 1980s were generating a roughly 50% effective yield or yield on cost.

(It's obviously more than that now.)

(To calculate the effective dividend yield, or yield on cost, take the current year's dividends and divide them by your original purchase price.)

So Buffett is now getting more than half his original investment paid back to him every year in the form of cash dividends.

The Problem with Dividend Growth Investing

So what's not to like about the DGI approach?

Owning a business that pays you 50% annual returns in the form of cash payments sounds pretty awesome, doesn't it?

The major drawback to DGI, of course, is that it's a horribly back loaded process. It literally takes decades for you to see those kind of outsized returns.

So, do you happen to have 3-5 spare decades in your investment horizon to wait for the 'ol compounding genie to finally squeeze his fat behind out of the magic stock market lantern?

I didn't think so.

Accelerating the DGI Process

But what if you could have it both ways?

What if you could experience the benefits of high quality dividend growth investing but without requiring a half century for it to really pay off?

What if there were a way to accelerate the process?

It turns out that the same solution to the value investor's lament - the difficulty in getting a low cost basis on high quality stocks - also addresses the DGIer's biggest hurdle.

If you recall from Part 2 of this series, I explained how I write puts on high quality stocks when multiple factors line up (I referred to my selection and set up process as my "strict underwriting standards").

This approach spins off a lot of cash which I accumulate and then use to fund, in whole or in part, the open market purchase of shares of my favorite stocks.

But because this cash doesn't come from or deplete my original capital, it's like I paid nothing for those shares acquired with that cash.

And when it comes to dividends, the math is simple, yet profound:

The lower your cost basis, the higher your yield. And the faster all your future dividend income and growth rates compound.

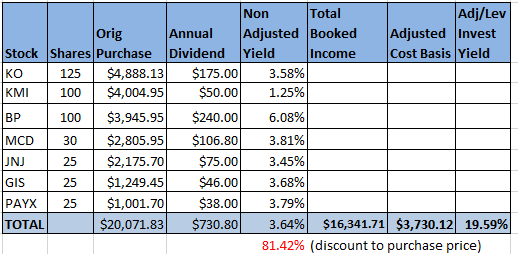

I shared this link with you yesterday, but here it is again - here are the current stocks I hold in the Warren Buffett Zero Cost Basis Model Portfolio along with the portfolio's overall adjusted cost basis and adjusted dividend yield.

{kind=link}

What kind of yields are you getting on your high quality stocks?

Options - Your Secret Weapon?

Options truly are like having a secret weapon.

The give the hare a second chance to catch up to the tortoise after realizing that for whatever reason - family obligations, personal hardship, lack of investing education, some less than ideal financial decisions in the past - he or she is losing the race.

And to a freakin' turtle!

I'm not talking about just any kind of option trading, of course.

I'm talking about specific, customized, structurally advantaged strategies designed specifically for dividend growth investors.

I'm talking about the specific, customized, investing- oriented strategy I teach inside The Leveraged Investing Club.

Tweet

Follow @LeveragedInvest

HOME : Dividend Stock Investing : Option Strategies for Dividend Growth Investors

![]()

>> The Complete Guide to Selling Puts (Best Put Selling Resource on the Web)

>> Constructing Multiple Lines of Defense Into Your Put Selling Trades (How to Safely Sell Options for High Yield Income in Any Market Environment)

Option Trading and Duration Series

Part 1 >> Best Durations When Buying or Selling Options (Updated Article)

Part 2 >> The Sweet Spot Expiration Date When Selling Options

Part 3 >> Pros and Cons of Selling Weekly Options

>> Comprehensive Guide to Selling Puts on Margin

Selling Puts and Earnings Series

>> Why Bear Markets Don't Matter When You Own a Great Business (Updated Article)

Part 1 >> Selling Puts Into Earnings

Part 2 >> How to Use Earnings to Manage and Repair a Short Put Trade

Part 3 >> Selling Puts and the Earnings Calendar (Weird but Important Tip)

Mastering the Psychology of the Stock Market Series

Part 1 >> Myth of Efficient Market Hypothesis

Part 2 >> Myth of Smart Money

Part 3 >> Psychology of Secular Bull and Bear Markets

Part 4 >> How to Know When a Stock Bubble is About to Pop